Intro to Gamma Scalping (Part 1 of 5)

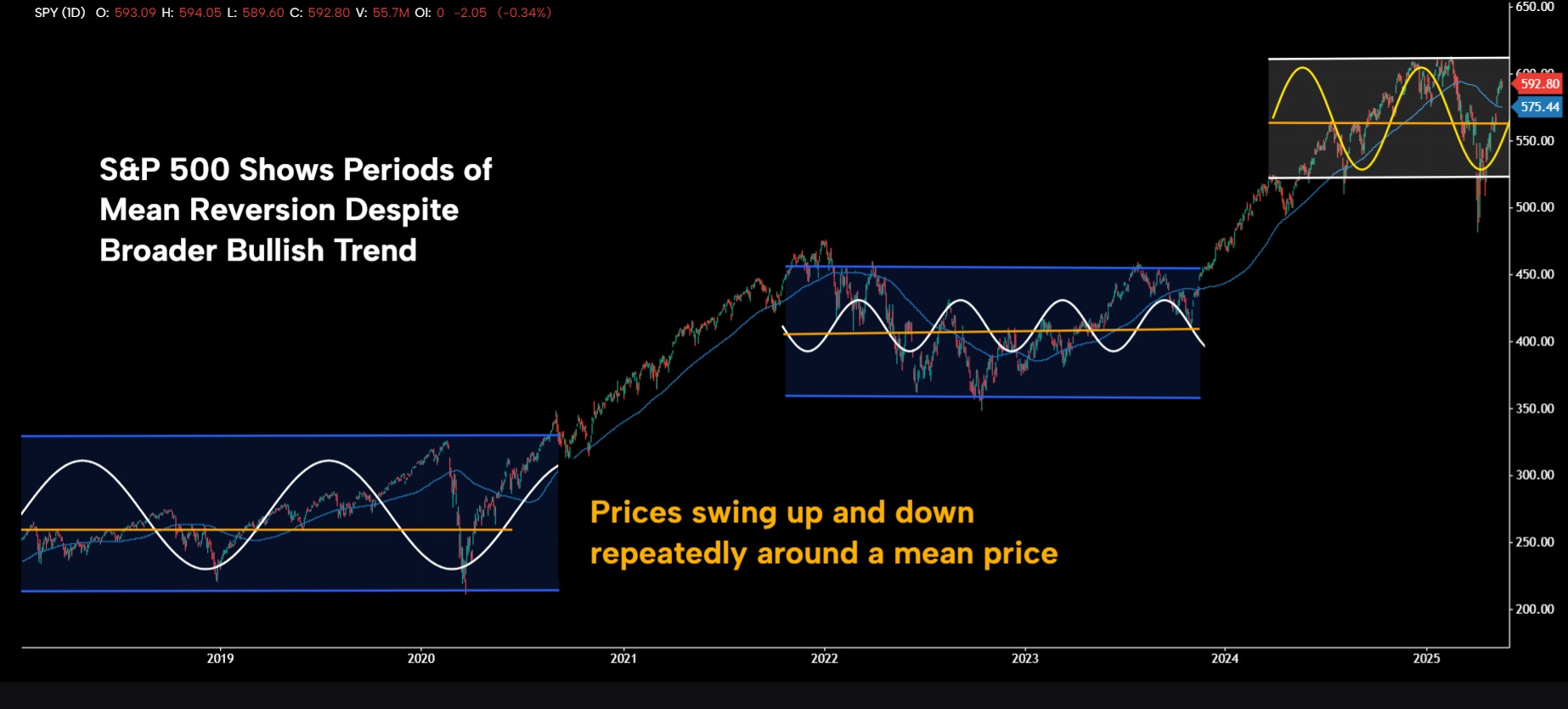

“Trend is your friend” is common advise. Only problem is that it is not always true. Markets do trend but not always. There are times when markets move in a zig-zag pattern. Such moves are also referred to as mean reversion.

Source: GoCharting

Mean reversion? In some ways, that's the opposite of trending markets. Each rise is followed by pull back. Once prices pull back, they rise back up only to fall again. That's different from trending markets where price movements are part of a consistent upward or downward trend.

CAN ONE NAVIGATE MEAN REVERTING MARKETS WITH CONFIDENCE?

In short, yes. There are many methods for navigating mean reverting markets. One of the compelling ones is to deploy gamma scalping.

WHAT IS GAMMA SCALPING?

Gamma Scalping is a trade set up combining a market-neutral options portfolio and then using futures and/or stocks to maintain market neutrality.

Market neutrality? A market neutral portfolio is unimpacted by underlying market moves. In theory, such a portfolio neither loses value from falling prices nor gains from rising ones.

However, in practice, such a portfolio is hard to construct as markets are dynamic, not static. But, in creating such a portfolio, investment managers can execute trades in a manner that results in consistent gains.

The process of maintaining market neutrality in an options portfolio through disciplined, regular, and consistent dynamic hedging is referred to as Gamma Scalping.

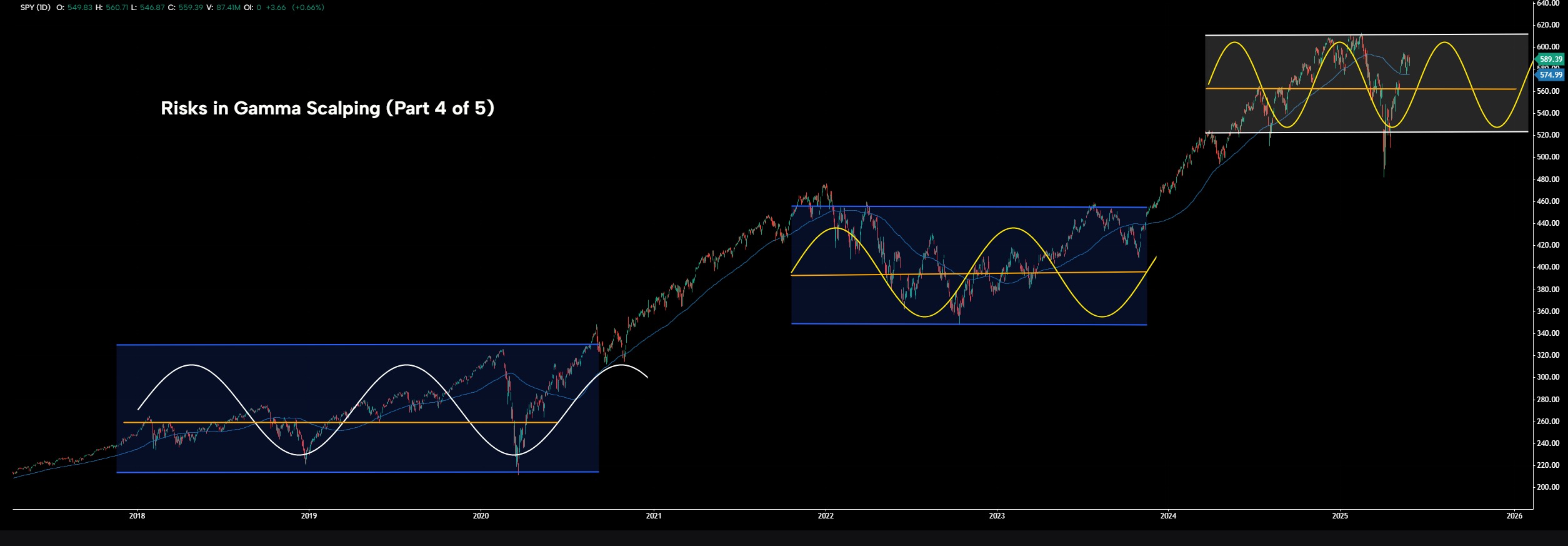

WHY GAMMA SCALPING NOW?

Times like now are when markets are prone to mean reversion than trend in one direction. Thanks in great part to the current US administration, policy flip flops are commonplace. Relentless supply of shocks & surprises constantly push & pull markets.

In current times, Gamma Scalping is one of the most methodical and systematic strategies for profitably navigating the market place.

IS GAMMA SCALPING A SILVER BULLET?

In short, No. There are no silver bullets in investing and/or trading. Gamma Scalping is not a silver bullet either. It is a compelling trading strategy, but not bullet proof and can result in losses.

Don't lose heart. There are clear conditions under which the likelihood of profitable Gamma Scalping increases. Scalping gamma under those conditions vastly increases the likelihood of profitable outcome. But as with all pursuit of returns, risks can only be reduced but not eliminated.

Being exposed to risk is quintessential but suffering losses is optional and can be reduced by taking intelligent risks.

CONDITIONS FOR GAMMA SCALPING TO BE PROFITABLE

For Gamma Scalping to be profitable, these five assumptions must hold true:

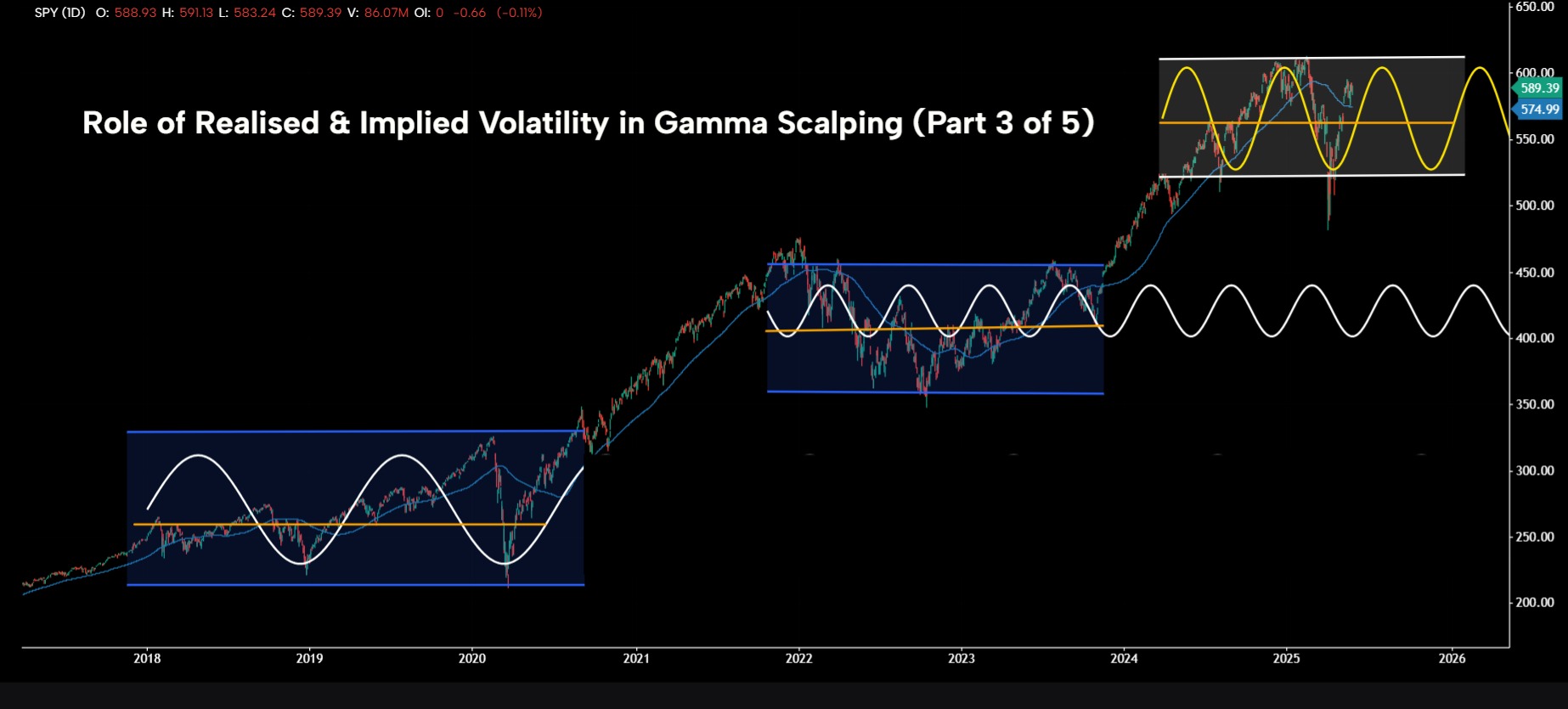

- Realised Volatility must be greater than Implied Volatility.

- Underlying Prices must exhibit mean reversion & not trend.

- Underlying prices must make sharp price moves & often.

- Underlying price at expiry to move past the break-even price points.

- Execute hedging trades to scalp gamma by neutralising delta at regular intervals.

The above are necessary, but for Gamma Scalping to be profitable, there should be more.

MECHANICS OF GAMMA SCALPING

This paper is the first of the five part series covering gamma scalping. There are multiple ways of scalping gamma. This paper shows the most common method. This section sets out the mechanics of scalping gamma in simple steps:

- Establishing a Delta Neutral Options Trade: Buy a delta-neutral long straddle (at-the-money long call

and long put at the same strike and expiry) with suitably adequate time to expiry. Short-dated options risk expiring worthless before the trader can execute gamma scalps. - Delta Neutral at Commencement: At-the-money (ATM) Calls typically have a delta of 0.5 and ATM Puts have a delta of -0.5 resulting in net delta of zero.

- Neutralising Negative Delta: When the underlying prices fall, the put delta becomes increasingly more negative inching towards -1. At the same time, the call delta becomes less positive and starts moving towards 0. This collectively results in negative delta at a portfolio level. To neutralise negative delta, the portfolio manager buys adequate futures at a lower price point relative to step (1) above. Net delta from the long straddle plus the delta from long futures should equate to zero to complete the first leg of gamma scalping.

- Neutralising Positive Delta: When the underlying prices rise, the call delta turns more positive inching towards +1 while put delta turns less negative inching towards 0. In aggregate, this results in a non-zero positive delta from the portfolio of options and futures. The portfolio manager will then be required to sell adequate number of futures contracts at a higher price relative to (3) and/or (1) above to reduce the delta down to zero.

- Continuous Gamma Scalping: A profitable Gamma Scalping occurs when steps (3) and (4) are repeated multiple times during the term of the options contract. Repeated buying of futures at lower prices followed by selling at higher prices or vice versa is necessary to recover the premium for the long straddle as described in step 1 above.

ARE THERE RISKS IN GAMMA SCALPING?

Gamma Scalping will result in losses if one or more of the following occur:

- Implied Volatility is greater than Realised Volatility.

- Underlying prices fails to exhibit mean reversion and instead tend to trend mildly.

- Underlying prices remain muted.

- Underlying prices at expiry stays well within the break-even range.

- Fail to execute gamma scalping trades to neutralise delta.

COMPREHENDING OPTION GREEKS IS ESSENTIAL TO SCALPING GAMMA

Option Greeks can be segmented into major and minor Greeks. Four major Greeks are:

- Delta: Measures sensitivity of option's price to underlying asset price. An option with delta of 0.5 will increase in price by USD 0.5 when underlying price increases by USD 1.

- Gamma: Measures option's delta changes when underlying asset price changes. An option with gamma of 0.1, its delta will increase by 0.1 when underlying price increases by USD 1.

- Theta: Measures option price’s sensitivity to time. All else being the same, if an option has a theta of -0.1, the option's price will decrease by $0.10 each day.

- Vega: Measures option price sensitivity to underlying asset's volatility. An option with Vega of 0.2, option price will rise by USD 0.20 when underlying volatility increases by 1%.

There are eight minor Greeks: Rho, Vomma, Vanna, Color, Lambda, Speed, Charm, and Zomma. These are useful but not essential for a basic comprehension of Gamma Scalping.

HYPOTHETICAL GAMMA SCALPING TRADE USING CME E-MINI S&P500 OPTIONS

The first step of Gamma Scalping requires establishing a long straddle. In the illustration below, we select a CME E-Mini S&P 500 Options expiring on 19th September 2025 at a strike price of 6050.

The 6050 call commands a premium of 207.12 index points while the 6050 put commands 237.92 index points in premiums aggregating to a total of 445.04 index points. In USD terms, this long straddle requires premium payment USD 22,252 (445.04 index points x USD 50 per index point) excluding transaction costs.

The delta at the inception of this contract is nearly zero at -0.01 with a gamma of 0.0014, vega of 27.366 and theta of -1.82.

Source: CME QuikStrike

MARKET DATA

CME Real-time Market Data helps identify trading set-ups and express market views better. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs https://deva.gocharting.com/cme .

DISCLAIMER

This case study is for educational purposes only and does not constitute investment recommendations or advice. Nor are they used to promote any specific products, or services.

Trading or investment ideas cited here are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management or trading under the market scenarios being discussed. Please read the FULL DISCLAIMER.

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by GoCharting. Read more in the Terms of Use.

↗ Related Analyses

Comments (2)

Loading comments…